Lifespan Insurance: A New Model for Promoting Long-Term Health

Prologue

Healthcare is broken. I learned this from work I did in the digital health space with Linda Avey, a co-founder of 23andMe. Linda had been on the founding board of Rock Health, the first digital health incubator, and we spent a lot of time at there working on digital health apps, talking with the Rock Health team, digital health founders, doctors, and healthcare analysts. One thing I found in these conversations was a prevailing frustration with the current system.

Everyone had their stories about the impediments that prevented progress and innovation. Doctors and workers inside the system complained about burnout, and sometimes a pervasive sense of fear and disempowerment, while even highly successful founders felt that it was difficult to bring models that would reduce cost to market. One AI innovator who directed a group of over 300 people at Google commented: “I’ve worked in many industries over my career, and healthcare is by far the worst”. You could guess how long a tech entrepreneur had been in healthcare by the depth of their 1000-yard stare. This journey of bleak realization is so common amongst digital health developers, it has become something of a meme:

Everyone seems to get that there’s something fundamentally wrong. Consumers and patients are frustrated too. When I first got involved, I thought the answer was technology, but, like many others, I’ve come to the view that the underlying problem originates with the incentives, and especially the payment system.

I had an idea 5 years ago for a new approach that could align the incentives between the consumer, the insurer, health innovators, and providers. I thought it was an obvious idea – or that it must have some conspicuous problems. I figured someone must be working on it, or that no one was for reasons that were lost on me, but lately I’ve been talking with health policy analysts, medical school founders and deans, doctors, and innovators, and their enthusiasm has made me think maybe there’s something to it.

What follows is a sketch of this idea, a new model I call Lifespan Insurance (LSI), which I hope can fix many of these problems by incentivizing and enabling the right behavior. LSI is a concept, not a fully fleshed out policy. The details are still a work in progress. I’d love to hear your comments on where the problems and opportunities lie. My hope is that a system like this can solve some of our biggest health challenges, while unlocking innovation, and improving the health of our fellow citizens.

Introduction

Current systemic challenges, including fragmented care, short-term insurance cycles, and misaligned incentives, highlight the need for a transformative model. The US spends almost twice as much per capita compared to other developed nations, while experiencing a ~5% lower life expectancy. Both of these metrics have been going in the wrong direction for decades, and medical expenses have become the leading cause of personal bankruptcy. Taking everything from people when they are at their most vulnerable sounds like a business model for organized crime, not healthcare. Clearly, we need to try something new.

Preventive care is systematically underused in our fee-for-service model, and represents an opportunity for routing around our sclerotic system of interlocking malincentives. A golden rule of innovation is to address areas that underperform on traditional metrics, but meet the needs of a new or underserved market. Preventive care, longevity, and wellness don’t fit well into our existing “sickcare” system, which is incentivized to treat illness. An insurance pool which has a relationship with a patient for 3.5 years (the average length of employment) has little incentive to pay for services that improve the customer’s health 5 years later, let alone in 10, 20, or 50 years.

Lifespan Insurance (LSI) aims to promote long-term health through preventive care and consumer wellness. Unlike traditional sickcare insurance, LSI is designed to reduce preventable disease over a consumer’s lifetime, and provides a framework which prioritizes patient-centered care, patient data sovereignty, innovation, convenience, and efficiency. It’s not that the existing system doesn’t provide some support for preventive care and wellness. It’s that the incentives aren’t there to drive robust innovation and usage. Good intentions can only travel as far as the lack of a business case permits. So we need to think seriously about how to pay for promoting long term health.

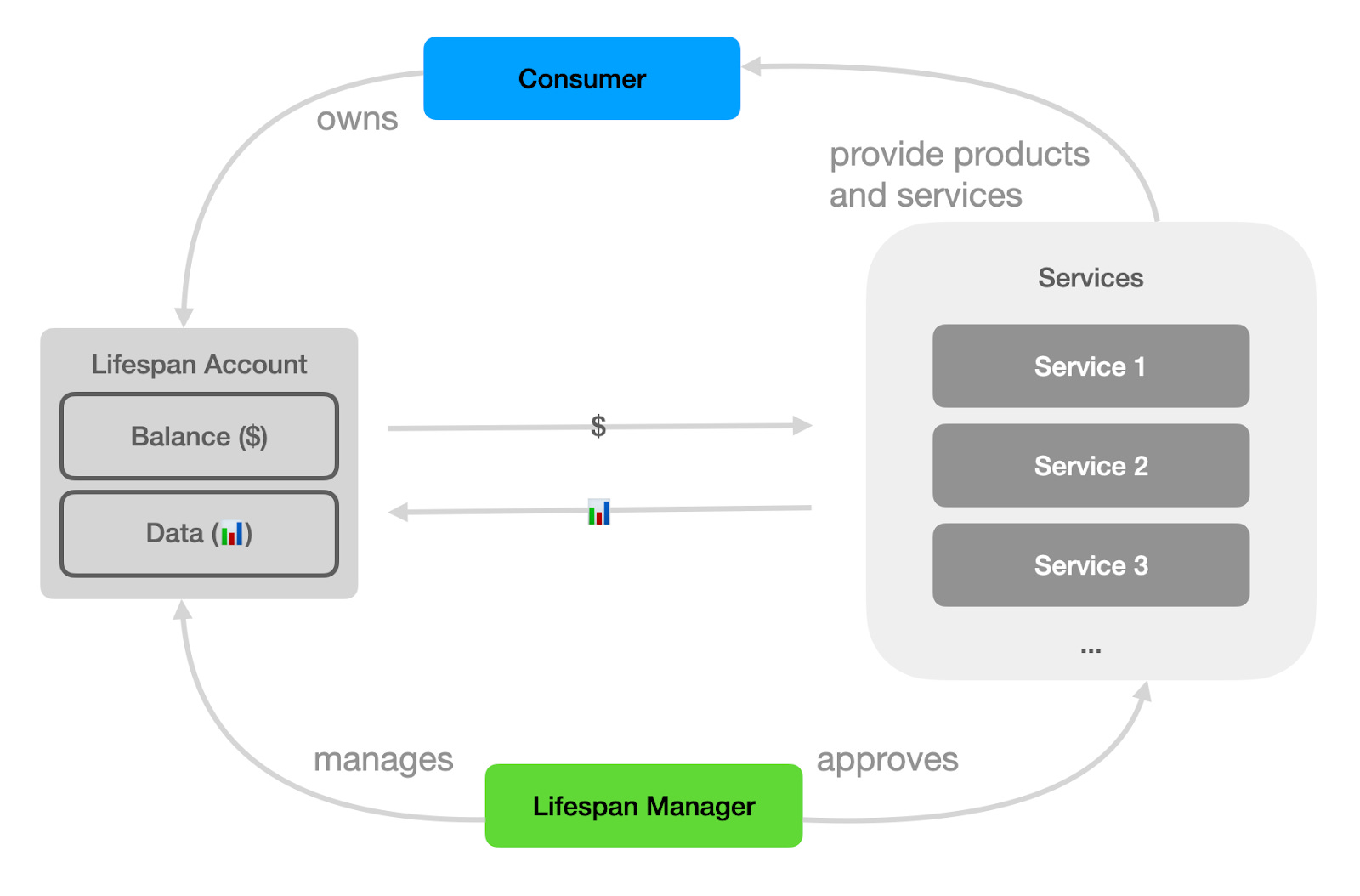

A key feature of LSI is the Lifespan Account (LSA). It combines a financial balance with a consumer’s health data, and is owned by the consumer for their lifetime. LSI creates incentives on both the consumer and their insurer to spend on services which reduce preventable disease, with the goal of promoting a long and healthy life.

Before we dive in, it may be helpful to enunciate some principles, and understand the challenges LSI hopes to address.

Problems with the Current Healthcare System

Short Term Commitment: Traditional employer-based insurance typically covers consumers only during the relatively short average employment period of approximately 3.5 years. This short-term focus disincentivizes investment in long-term preventive treatments and overall health. ICHRA has mitigated this somewhat, and I discuss it in a later section.

Data Fragmentation: Health data is often trapped within silos across multiple insurance plans, healthcare providers, and digital health services, limiting the potential for comprehensive health management, and data analysis. Data fragmentation is such a severe problem in the existing system it has created a whole ecosystem of companies, and data standards which try to address the problem. Nonetheless, a common refrain is that the data is difficult to access because the major EMR companies jealously guard access to what they view as their asset.

Consumer Disempowerment: Employer-based insurance plans are an example of the principal-agent problem. Plans are selected by human resources departments (which often lack the training to make healthcare buying decisions), removing consumer choice, and distorting natural market dynamics. This has been mitigated somewhat by the Affordable Care Act (ACA), but innovation has been modest.

Market Consolidation and Oligopolies: Comprehensive insurance plans incentivize health insurers to consolidate healthcare services, reducing consumer choice and creating oligopolies that control access to clinics and care providers. This is compounded by employer based insurance which must select insurance plans that cover all their employees.

Doctor-Centered Care: The central role of doctors in delivering and approving care for individual patients is deeply baked into our regulatory and billing frameworks, despite the lip service the industry gives to patient-centered care. This model fosters inefficiencies through increased labor costs, inconvenience due to scheduling and travel, and administrative burden. McKinsey found that hospital and doctor costs accounted for 85% of the $477B excess spending costs in the US compared to other nations.

Lagging Practice: Since doctors are incentivized to use their time creating billable events, while spending time on research and keeping up to date is an unwelcome cost to their business. As a result, it takes 14 years on average for clinical findings to be integrated into routine medical practice.

Billing Codes: The AMA, which represents the interests of doctors, also controls billing codes which determine what services can be paid for. Billing codes incentivize health care services to maximize transactions rather than seeking long term wellness. It takes 1.5 to 3 years to get new billing codes, and applications can cost hundreds of thousands of dollars. Since one of CMS’s requirements for new billing codes is widespread adoption, the existing system creates a Catch-22 that interferes with getting innovations to market. In effect, our government’s approach prioritizes paying for what the medical community happens to do rather than what science, technology, and innovation can enable.

Illness-Driven Financial Model: The current system financially rewards treating sickness rather than preventing it. The ACA requires insurers to cover certain preventive measures, however, uptake has been low, possibly due to the short term commitment problem (#1 above). Credible analyses by the CDC, NIH, and leading research groups indicate that broad preventive health measures could save on the order of 5–15% of U.S. healthcare spending – up to $500B annually. The Milken Institute found the US could save $271B in productivity losses through preventive health.

Labor-Intensive by Design: Regulatory frameworks often require that even routine, low-risk care decisions be made or approved by licensed medical professionals. This mandates the use of highly trained—and expensive—labor for tasks that could be safely handled by digital systems or less credentialed providers. As a result, healthcare has become a high-labor sector with limited productivity growth, making it especially vulnerable to Baumol’s cost disease—a structural force that drives prices up faster than efficiency can improve.

These interlocking problems have created an industry that seems impossible to fix, despite numerous attempts. U.S. healthcare spending keeps rising faster than inflation, and GDP. Costs now exceed 17% of GDP and are projected to surpass $7 trillion by 2031. This surge isn’t due to better outcomes and cannot be entirely attributed to an aging population—it’s driven by administrative bloat, regulation that prevents automation, pricing power, and structural inefficiencies that make the system fundamentally unsustainable. I’m part of a fund that invests in tech driven health and life science, and this is one of the reasons we have a bright line against investing in companies which support this business model. The change we need must come from a fundamentally new place.

Components of Lifespan Insurance

The LSI model introduces several concepts that work together. I’ve already discussed the Lifespan Account (LSA), which combines funds and health data centered on an individual consumer. This is managed by a new type of healthcare entity, which acts as both payer and recommender of services, called a Lifespan Manager (LSM). The consumer chooses an LSM to manage their account (LSA). The LSM recommends and pays for Lifespan Services using the account balance. Services provide health-promoting products and services to the consumer and contribute data to the LSA. Unlike traditional health insurers which gate access to services, LSMs actively recommend and pay for services that will reduce later spending out of the account.

This is the key idea behind LSI – the Manager benefits in the long run if the services they recommend reduce overall costs. I’ll get into this in a later section. But first, here is a glossary:

Consumer: An individual who participates in LSI.

Lifespan Manager (LSM): A business which acts as a custodian and manager of consumers’ Lifespan Accounts. LSMs offer personalized health guidance, pay for services, and aggregate and analyze health data.

Lifespan Account (LSA): Maintains a financial balance and health data. Owned by a consumer who has a right to transfer it between Managers.

Lifespan Account Data: A continually updated record of health metrics, diagnostic results, wearable outputs, and clinical interactions. Services contribute health data to the consumer’s LSA as part of the arrangement with the Manager.

Lifespan Account Balance: A dedicated financial account which accrues value through contributions by the consumer, employers, public programs, and insurers. Funds from the account can be used on preventive health services.

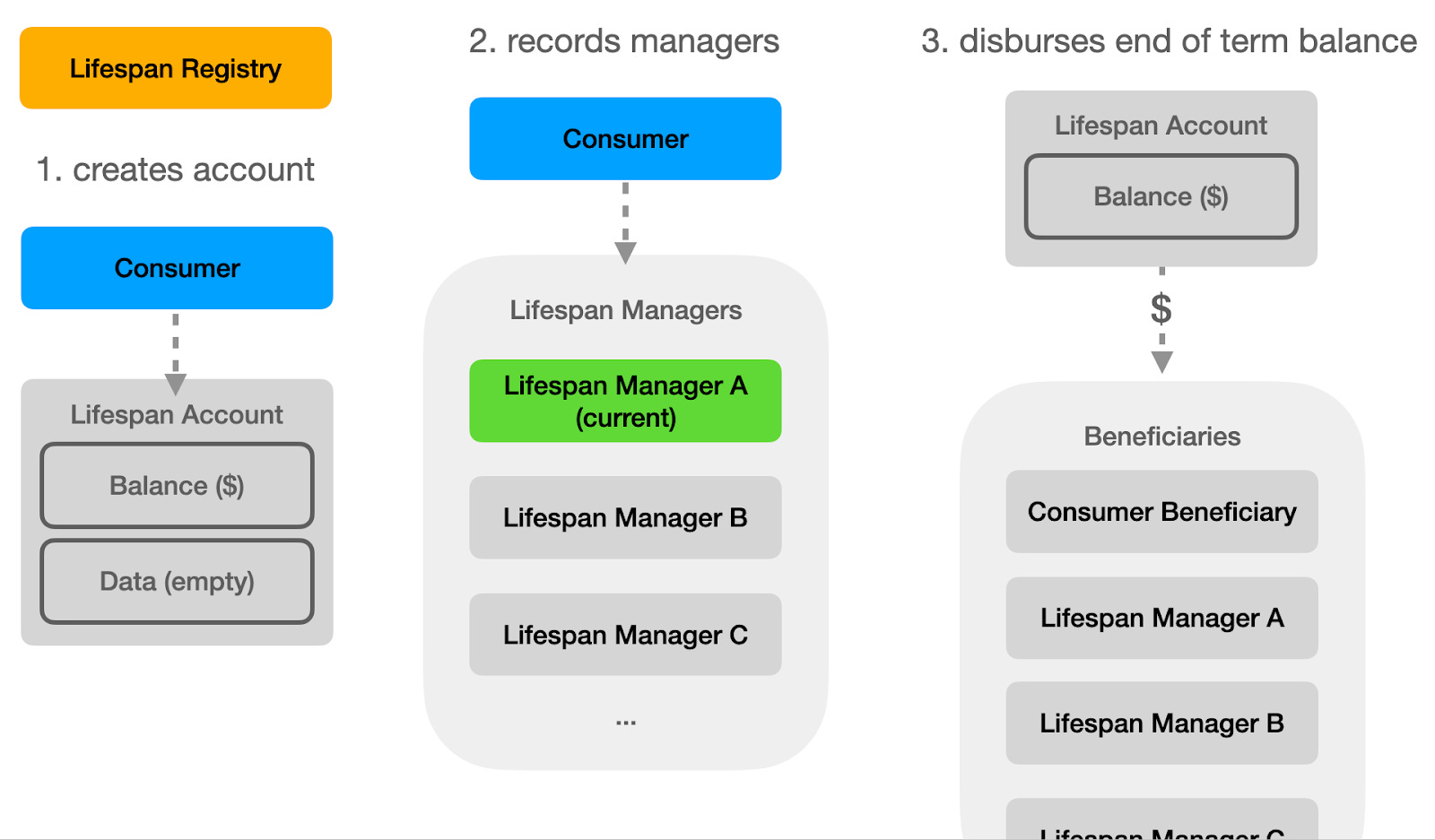

Lifespan Registry (LSR): A Lifespan registry creates LSAs and manages the distribution of funds to LSMs that have managed the LSA, at the end of the LSA’s term. In principle, this is a largely automated service where LSMs and consumers register the consumer’s acceptance of an LSM for their Account.

Lifespan Service (LSS): Provide products and services to consumers. LSMs pay for services out of a consumer’s Account. Service companies may include consumer health applications, preventive health coaches, gyms, supplements vendors, fitness studios, and even grocery stores. In principle any product or service an LSM determines can reduce preventable health costs might be a Service.

Incentives

Our journey through life includes many choices that affect our health. Focusing on prevention early can reduce the cost of disease treatment later. LSI is designed to provide transparency, and evidence-driven advice to consumers to make the most cost-efficient decisions with respect to their long term health.

Both the LSM and the consumer have an interest in preserving the balance in the consumer’s LSA because each receives a portion of the balance when it terminates. In the case of the consumer, this may be at the end of life, and the value is inherited by their descendants, or the consumer may choose to cash out, perhaps according to certain age-based rules, or with a penalty, like life insurance. This aligns the consumer with their LSM, since both have an interest in maintaining the balance. The LSM also has an interest in the consumer living a long life, since they receive a subscription payment for maintaining the account and providing health advice. Thus, the LSM is motivated to discover and suggest preventive services that will reduce overall healthcare costs for the consumer.

The Account accrues value through contributions from the consumer, employers, government services like Medicaid, or traditional healthcare insurers. Each of these has their own natural incentives for funding a consumer’s LSA.

Consumers: The LSA ought to provide similar tax sheltered benefits to an HSA, so the consumer has a direct interest in spending on Services through this account. The consumer also benefits from the health suggestions of the LSM, and the centralization and analysis of their health data.

Employers: Preventive health has been shown to increase employee productivity, leading to 27% fewer sick days (WHO Report 2017), higher retention, engagement and morale, and saves on their healthcare costs. The proliferation of employer-based preventive health programs creates a challenge for HR departments tasked with purchasing benefits for employees. This results in one-size-fits-all benefits. Contributing to an LSA and allowing the employees to choose an LSM that suits them separates the responsibilities properly. The employer could offer an LSM contribution as a benefit, and might even recommend an LSM that aligns with its business. The LSM takes the place of the HR department, using robust data and analytics to make personalized service recommendations to each employee.

Government: Medicaid has an interest in reducing the overall cost of preventable disease, so funding LSAs makes sense from a public health perspective. In addition, Medicaid and other government programs can later use LSAs to recover some part of disease treatment cost, creating the appropriate incentive on LSMs to reduce these later costs by spending on early prevention.

Private Healthcare Insurance: Traditional sickcare insurers could fund the LSAs of enrollees and gain the right to charge some fraction of the costs of preventive care to them, as discussed later in this section. The government may have an interest in requiring sickcare insurers to do just this, just as it now requires them to provide certain free preventive health services.

So, as we can see, the Account is used to pay for both preventive services and treatment for preventable disease. Effective early prevention should reduce the need for treatment later, so LSMs succeed financially when they motivate consumers to purchase and use the right preventions. However, this motivation only works if the Account bears some part of the cost for treatments for preventable disease.

So how can treatment costs be applied to the LSA? The simplest approach is simply to allow the LSA to be used to pay for out of pocket expenses on the theory that out of pocket expenses like copays for doctors’ visits and prescriptions will be less for healthier patients. This will be familiar to individuals who have used Health Savings Accounts (HSAs). This approach is easy to understand and implement, but other mechanisms that more tightly couple preventable disease costs to the LSA may be a more powerful way of driving the right incentives.

Another approach is to allow or require traditional sickcare insurers to participate in LSI, for example by both contributing to LSAs for prevention and extracting costs from them for preventable disease treatment. Thus, as patients use different sickcare insurance throughout their lives, these insurers would collectively share in the cost and benefit of LSI. Thus, LSI acts as a kind of preventive care reinsurance program, but with the benefit of incentivizing the consumer and aggregating long term health data.

The Lifespan Registry

An LSM is incentivized to keep customers for life, for both subscription fees and to maximize its share of the final LSA balance. Since customers can switch their LSM, a means for tracking each LSM’s contribution to the customer’s LSA is required. This is the role of the Lifespan Registry (LSR). This is a class of companies which are authorized to create and track LSAs. An LSR is a simple service that generates LSAs, and permits a consumer to assign their LSA to an LSM. At the end of the Account term, the LSR distributes the balance to the consumer (or beneficiaries) and LSMs according to some formula (for example, number of days managed). The precise percentage of the remaining balance distributed to LSMs, and the cost of subscription will require analysis, and remains a key question for LSM financial models.

Challenges

Out of Pocket Costs

Determining which services provide real long-term value is a key challenge for the LSI model, and might put them on the opposite side of the table from the consumer. For example, the American College of Radiology argues the benefit from whole-body MRI scans in healthy people isn’t worth the cost. Yet, MRI scans are becoming increasingly popular in direct to consumer offerings. Would LSMs approve payment for such services? If so, at what cost? Arguably, the incentive structure of LSMs could resolve this issue. Since LSMs are incentivized to maximize the account balance (which also benefits the consumer), they may decide not to offer such services, or to offer them with a discount that would then create positive long term value for the LSA. It would then be the consumer's choice to cover the unsubsidized portion as an out of pocket expense, offering a balance between consumer choices and the recommendations of an LSM’s actuarial tables. On the other hand, services with unambiguous long term value like DEXA scans, and colon-cancer detecting kits would be covered in full, and promoted to the consumer.

Dealing with Cost-shifting

Another issue with integrating Lifespan Insurance with the existing healthcare system is ensuring that traditional sick-care insurers don’t offload costs onto the consumer’s LSA by simply refusing to pay for services. For example, if a patient elects for an early intervention that falls into a gray area between diagnosis and prevention, a sick-care insurer might deny coverage, hoping the cost will be picked up by the LSI account instead. This creates misaligned incentives and threatens the sustainability of the LSI model. Fortunately, similar problems have been tackled before in the world of supplemental insurance. Coordination of Benefits (COB) rules are routinely used to determine financial responsibility between primary and secondary insurers. Independent Dispute Resolution (IDR) processes—now mandated under federal law—allow for structured negotiations when payment disputes arise. Some states have gone further, requiring insurers to disclose denial rates and imposing penalties for bad-faith denials. These tools offer a clear roadmap for how LSI can defend against cost-shifting tactics and maintain focus on its mission: investing in prevention to reduce long-term health costs.

I hope this discussion shows how LSI’s different entities – the Account, the Registry, and the Manager – work together to create an environment that preserves consumer choice, drives good health decisions, consolidates data, and promotes competition.

Data Sovereignty and Aggregation

I take it as a fundamental principle that consumers should be in control of their data. While HIPAA was intended to achieve this, in practice patients struggle to retrieve records from their traditional healthcare providers. In addition, with the proliferation of direct to consumer digital health, health data is scattered amongst many different private silos. Currently, there is little incentive for these companies to pool their data. LSI provides a clear incentive – LSMs offer digital health services the opportunity to reach new customers in exchange for contributing the data they produce to the patient’s LSA.

The LSI model naturally aggregates health data into the consumer-controlled Account. These datasets will be a critical asset for public health, drug discovery, and consumer and digital health insights. LSI customers could opt-in to allowing their anonymized data to be used for research purposes, or, perhaps, to be contacted for clinical trials.

Data sovereignty means consumers should be able to move their account easily between LSMs. Raw data acquired by LSMs should be copied directly into the consumer’s account, perhaps in a simple standard format, recording the data and the Service from which it was collected. When the consumer chooses to switch LSMs, they should be able to do so by simply transferring this record and the financial value to the management of the new LSM. In addition the LSM should be empowered by regulation to request consumer health data from traditional healthcare entities. In this way, the LSA can emerge as the personal health record that the industry has long discussed, but never achieved.

Trust and Privacy

For Lifespan Insurance to succeed, consumers need to trust that their health data is secure and used only with their consent. Control over LSA data should rest entirely with the individual—it’s their information, not a corporate asset. Companies that access or manage this data, especially LSMs, must follow clear rules that prohibit sharing or selling it without the user’s explicit permission. Firms involved in surveillance should be strictly barred from the LSI ecosystem. Following the approach of HIPAA, LSA data should be stored separately from personally identifiable information, however, this should only be applied to the aggregate data, not to the Services. HIPAA regulations applied to service companies would prevent an enormous number of valuable consumer services from providing value in this space. These protections should be backed by enforceable policies, as well as strong whistleblower incentives to surface any violations. The goal is to make it clear: this system is designed to serve the person, not to exploit their data.

Why Digitally-Driven Health is Essential

Preventive care, unlike acute treatment, must reach everyone—across decades—not just the sick or injured. That means it has to be delivered efficiently, at scale, and at a fraction of the cost of traditional care. The legacy system—doctor-centered, appointment-based, and expensive—is fundamentally unsuited for this. Digital care isn’t just a good option; it’s the only infrastructure that can make prevention both affordable and effective.

Cost and Scale

Clinical medicine results in scarcity and increases costs. Every interaction requires a licensed provider, a facility, scheduling, and paperwork. Preventive health, by contrast, should be abundant. Apps, wearables, AI triage, and telehealth services offer a way to deliver guidance and monitoring continuously, cheaply, and with far less friction. A 2021 McKinsey report estimated that up to $250 billion of U.S. healthcare spending could be shifted to virtual care, with telehealth alone saving $17 billion per year. Deloitte has found that digital tools can reduce hospitalizations by 20% and improve adherence to preventive regimens by 60%.

Keeping Up with Science

Traditional medicine is slow to adapt. Studies show it takes more than a decade for clinical research findings to become standard practice. Updating traditional medicine isn’t just slow, it’s expensive. Pharmaceutical companies spend over $20 billion each year marketing to doctors—far more than they spend on R&D. The result isn’t just inefficiency; it’s a distortion of care decisions, biased toward marketing drugs over evidence-based strategies. LSI flips this logic: instead of marketing to doctors, it incentivizes LSMs to use data science to optimize outcomes. LSMs deploy system-wide changes to preventive protocols based on evidence, not ad budgets, and can update digital guidelines instantly, without retraining an entire workforce.

Lower Regulatory Need than Sickcare

Preventive care usually doesn’t involve life-or-death emergencies. It’s about routines: reminders to schedule a screening, track your steps, refill a prescription, check your glucose, or follow a diet. These are exactly the kinds of interactions that digital platforms excel at. AI can parse many health signals in real time and generate personalized suggestions, while human care teams focus on edge cases and higher-risk patients. The labor burden is shifted to machines—and the care becomes more continuous and accessible.

Personalized Health at Scale

Traditional medicine relies on population-level guidelines. LSI enables precision. By aggregating an individual’s Lifespan Account Data—lab results, activity levels, sleep, food logs, biometric trends, microbiome analysis, genetics, etc.—LSMs can deliver truly personalized preventive plans. These systems learn and improve over time, tailoring recommendations to what actually works for each individual.

And consumers are ready. Over 50 million use wearable devices. A Rock Health survey found that 80% have used digital health tools, and 70% are comfortable sharing data with tech companies if it leads to better care. The infrastructure and user base are already in place.

For LSI to work, preventive care must be continuous, personalized, and inexpensive. That means digital-first by design. Digital tools make LSI viable—not by replacing doctors, but by letting them focus where they’re needed most, while the LSI preventive health system runs quietly, efficiently, and automatically in the background. Without digital infrastructure, prevention stays stuck in the 20th century—underused, expensive, and generic. With it, we can make long-term personalized health guidance accessible to everyone.

Enabling AI-Driven Diagnosis

Regulatory capture has enshrined the idea that one must always “talk to your doctor”, but numerous studies have shown that AIs are consistently outperforming doctors in many areas of diagnosis, including dermatology, rash diagnosis, chest x-rays, pathology, and routine high volume diagnosis. A study published in Nature showed that patients find AIs to be more empathetic than human doctors. A systematic review and meta-analysis found that there was no significant difference between AI and non-expert physicians, though it lags behind specialists in complex multimodal cases. In other words, AI excels in routine care, which is exactly what we find in a preventive medicine context. Anomalies can be flagged and raised to a human doctor. It is a common refrain that AI is currently the worst it will ever be, so now is the time to prepare for a new world of AI-driven medicine. LSI offers an opportunity to pilot this important technology and focus it where it’s needed most and best suited: routine care.

Medical Education: Clinical Science Engineers

The digital health industry has already highlighted a need for a new class of data scientist-medical professional. Medical schools are already seriously discussing the need to shift medical education to get ready for a world of AI, internet driven care, and data at scale.

LSI will accelerate the need for a new class of professionals who understand digital systems, big data, consumer engagement, and public health: Clinical Science Engineers. In the workforce, whether in digital health companies or as product managers and research scientists at LSMs, they will engage constantly with the latest clinical research, have access to large digital datasets, and will have the training to make data-driven decisions about diagnostic and treatment plans, and to manage change in software systems. Because of this, Clinical Science Engineers will be much better informed than most doctors on optimal medical decision trees. Regulatory bodies should confer on them a status analogous to doctors, enabling them to create and modify diagnostic and treatment plans – and apply them to digital systems without onerous regulatory overhead for every change. Doctors don’t apply to the FDA for every change they make to a treatment plan. Neither should this new class of digital health professionals.

The LSI Ecosystem

One of the exciting aspects of LSI is how it encourages a wide range of new participants to provide health-promoting products and services. The LSI ecosystem isn’t limited to doctors, hospitals, or digital health tools—it can encompass an entire marketplace of services that contribute to healthier, longer lives.

Because LSMs are paying directly from the consumer’s account and stand to benefit from improved outcomes, they’re motivated to rigorously verify which services actually deliver health benefits. This creates a dynamic market of preventive health innovation—where digital health tools, mindfulness or alternative and functional medicine providers, food companies, and fitness companies all have a clear path to participate, so long as they can prove they work. Rather than relying on government mandates or employer-driven wellness programs, LSI helps consumers choose from an ecosystem of health interventions. Because LSMs consolidate consumer demand and align with their interests, they play a role both as health experts and consumer-advocates, driving the market to produce cost-effective products that provably improve long term health.

Lifespan Managers form the hub of the LSI ecosystem. To Service companies they offer an important marketing channel. Instead of business development targeting a vast number of employers through overwhelmed and underinformed HR employees, Services would make their case to a smaller number of specialists in LSMs. In turn LSMs would market themselves directly to consumers, or to employers. Different LSMs might specialize in different aspects of care. I can imagine LSMs specializing in services for women, another for men, employees, rural and underserved populations, or even for infants.

Because LSI offers a general model for tackling problems where long term outcomes are important, we can even imagine them extending into other areas where a transactional payment model creates malincentives. One example is homeless care. Cities tend to contract nonprofits with little long-term accountability for client outcomes. Homeless clients who recycle back to the street represent a future profit for such services, creating a malincentive similar to that in the sickcare system. An LSM focused on this population could act as a highly incentivized care coordinator. I don’t have a clear sense of whether homeless care should be included in LSI, but I offer this example to expand our imagination for what LSI could do.

Existing digital health and scientific efforts are well positioned to forge a path as LSMs. Function Health has built a growing consumer business around blood tests, and they recently acquired Ezra, a low cost whole-body MRI imaging company. They are planning to expand their operation to new forms of testing, providing long term functional health advice to their customers. Dr. Leroy Hood and Nathan Price, pioneers in systems biology, have proposed the concept of Scientific Wellness, which is a proactive, data-driven approach to health, focused on maintaining wellness rather than reacting to disease. They propose a “resilience score” that incorporates high-dimensional biological data (genomics, proteomics, metabolomics, microbiome, etc) to identify disease risk early and optimize wellness continuously. I expect that there will be many different approaches that could compete to provide value within the LSM framework. While internal metrics like a resilience score can help individual LSMs guide their customers on a path to wellness, it will be important to provide visibility into overall metrics of LSMs so that consumers can make informed choices.

Apple has emerged as a leading company constructing a personal health record. Their HealthKit service provides a useful way for consumers to aggregate their health data. Apple and other tech behemoths have ambitions to build a personal health record and make themselves a center point in the health system of the future. While Apple’s commitment to privacy is laudable, a personal health record based on a business model predicated on locking people into a proprietary digital ecosystem works against the principle of consumer data sovereignty. Apple could play an important role as a leading LSM. They would have to give up their control over consumers’ digital health records, however.

Many companies, especially in tech, aim to build proprietary ecosystems that lock in users by capturing and retaining their data. This approach is often seen as a competitive advantage—a “moat” that protects business interests and boosts investor appeal. In digital health, the same logic has led to platforms that silo patient data in closed systems, each hoping to become the central hub for healthcare. But this model is fundamentally at odds with public health goals. Health is too multifaceted for any single company to serve all needs effectively, and fragmenting data across corporate silos leads to inefficiencies, duplicative care, and poorer outcomes. Worse, oligopolies owning healthcare data will drive up costs, and amassing massive sets of proprietary health data would create barriers to future innovation. LSI addresses this by putting the consumer in control of their health data and enabling portability across services—ensuring that information flows where it’s needed, not just where it’s captured.

What We Need from Government

The Lifespan Insurance model doesn’t require tearing down the current system – in fact it works in tandem with it – but it does need some targeted regulatory changes to work. These changes are mostly about creating space for a new kind of entity to operate, allowing for a payer-manager. It’s possible that by reducing the scope of services I imagine, LSI could get off the ground without regulatory changes.

First, we’ll need to recognize Lifespan Providers (LSMs) as a new type of healthcare organization. They’re not insurers in the traditional sense, and they’re not care providers either. They manage a consumer’s Lifespan Account, make recommendations, and pay for preventive services. There may be regulatory changes required to allow them to receive contributions from employers, individuals, traditional insurers, and government programs, manage those funds, and contract with a wide range of services—including digital and non-traditional providers. Medicare Advantage and Accountable Care Organizations offer some precedent here, but LSMs might need clearer authority to operate as long-term preventive care managers.

Second, Lifespan Accounts (LSAs) ought to be treated like tax-advantaged accounts. Right now, Health Savings Accounts (HSAs) are the closest analog, but they come with restrictions that don’t make sense for LSI. LSAs should allow contributions from multiple sources and be usable for a broad range of preventive services. This includes digital tools, nutrition programs, wearables, and even things like gym memberships or supplements if there’s a reasonable case that they improve health outcomes. These accounts should follow the consumer through life and be transferable to different LSMs, with clear rules around qualified spending.

Third, health data regulation needs to move beyond just access and toward true portability and ownership. The 21st Century Cures Act and FHIR standards point in the right direction, but in practice, data is still fragmented and hard to move. For LSI to work, consumers need the ability to direct all health-related data—whether from a clinic, a wearable, or a health app—into their LSA. That means requiring LSSes to contribute data to consumers’ accounts. This could be a simple API standard that would enable any LSM to capture data from any Service that participates.

Fourth, the LSI model eliminates the need for billing codes. Instead of reimbursing each transaction, LSMs make decisions about what to pay for based on value and expected impact. This simplifies the system, removes a major barrier to innovation, and cuts down on the administrative burden that dominates traditional healthcare. To support this, regulators may need to allow entities like LSMs to operate outside the fee-for-service billing code framework, for example, when they’re recommending regulated services to a consumer.

Fifth, we should resist the attempt to create too many standards. Unlike transactional models, LSI naturally incentivizes participants to do the right thing. The government should not be over-prescriptive about how LSMs achieve their goals. While certain types of healthcare metrics might be useful, like the resilience score, ideas like these should be left up to the market. If LSMs do a good job and choose the right metrics, they will naturally profit.

Finally, the government needs to remove barriers to digital guidance and AI-driven health advice, including the ability to rapidly iterate on software without triggering onerous medical device approvals. LSMs will rely on software systems to analyze data and recommend preventive actions. Because these services are delivered in a preventive context, they don’t need to be regulated like drugs or high-risk devices, but they do need to meet standards for transparency, accuracy, and patient consent. The FDA has already begun to define this space, but further clarity—especially for systems used in non-clinical, preventive contexts—would help. Regulatory sandboxes, similar to those used in fintech, could allow new models to be tested safely before broader rollout.

Taken together, these changes would give Lifespan Providers the space and tools they need to operate. They would also modernize parts of the healthcare system that are already overdue for reform—data access, spending flexibility, and overreliance on billing codes. The goal isn’t to replace what works but to open a lane for something better.

Comparison with Existing Models

While Lifespan Insurance is an ambitious proposal, it is related to existing, proven mechanisms that suggest its plausibility and potential. The concept of a dedicated account for health-related expenses is not entirely new. Health Savings Accounts (HSAs), for example, offer consumers tax-advantaged accounts they can use to pay for qualified medical expenses. Like the Lifespan Account (LSA), HSAs are individually owned and portable. However, they fall short in several key areas: HSAs are tied to high-deductible health plans, lack integration with health data, and are not designed to support or incentivize preventive care across a lifetime. HSAs are passive repositories of funds, while LSAs are intended to be active, intelligent, and integrated components of a lifelong health strategy.

John Hancock’s Vitality Insurance

A more direct precedent for LSI’s approach to incentivizing prevention can be found in John Hancock’s Vitality Program. Vitality pairs life insurance policies with wearable technology and behavioral incentives. Consumers are rewarded for healthy activities such as exercise, check-ups, and dietary improvements, often receiving discounts on premiums or other financial rewards. The success of this model demonstrates several important points: consumers are willing to share health data in exchange for financial benefit; preventive incentives change behavior; and insurers can benefit financially from improved consumer health.

However, Vitality’s model is limited in scope. It operates within the boundaries of life insurance, does not integrate with healthcare providers or medical spending, and offers no mechanism for long-term health data aggregation or service reimbursement. In contrast, LSI aims to create a complete ecosystem—one that not only tracks behavior but actively funds and directs preventive services through a unified account and health record. While Vitality nudges consumers toward wellness within a single insurance product, LSI creates a foundation for a lifetime of personalized, incentive-aligned healthcare management.

Medicare Advantage

While both Medicare Advantage (MA) and Lifespan Insurance (LSI) aim to align healthcare incentives with better outcomes, they differ in a core structural way: MA is a late-stage care management system, whereas LSI is a lifelong prevention system. MA begins at age 65, by which time many chronic conditions are already entrenched. It uses capitated payments to encourage cost-efficient care, but its scope is limited, and the incentive to invest in long-term health is inherently weak. If an MA enrollee switches plans—as they can during annual enrollment periods—any prior investment a plan made in that person’s future health walks out the door with them. In contrast, LSI is built for true continuity and alignment: it begins at birth and follows the consumer throughout life. Lifespan Providers can be changed at any time, but because each provider’s contribution to long-term health is tracked and tied to the consumer’s Lifespan Account, they still share in the outcome. This ensures that preventive investments are rewarded, even if the consumer switches providers—creating far stronger, longer-term incentives than are possible in MA. LSI thus combines the stability of lifetime alignment with the freedom of consumer choice, enabling a truly prevention-first healthcare model.

ICHRA

ICHR (Individual Coverage Health Reimbursement) is a federal program that allows employers to reimburse employees tax-free for individual health insurance premiums and qualified medical expenses, instead of providing a traditional group health plan. ICHRA gives employees more flexibility to purchase ACA-compliant health plans but does little to change how care is delivered or incentivized. It offers no mechanism for proactive prevention, no long-term alignment of incentives, and no integration of personal health data. By contrast, LSI is specifically designed to promote lifelong health, with a persistent account, portable data, and aligned incentives that encourage investment in preventive services. While ICHRA shifts who pays for care, LSI rethinks why and when care is delivered in the first place. LSI could be framed as an extension of ICHRA focusing on incentivizing long-term preventive health.

Other Trends

The feasibility of LSI is further supported by growing momentum in digital health, value-based care, and health data interoperability. The proliferation of wearable devices, telehealth services, and consumer-driven healthcare apps shows that patients are ready for models that prioritize convenience, personalization, and control. Policymakers and payers have also signaled interest in moving away from fee-for-service and toward outcomes-based models, which aligns directly with the incentive structure of LSI. Finally, the increasing public and institutional demand for greater health data portability—bolstered by the 21st Century Cures Act and FHIR API standards—makes the idea of patient-owned, longitudinal health records more technically feasible than ever before.

LSI is not a radical departure, but a coherent synthesis of models and technologies that already exist. It combines the financial autonomy of HSAs, the behavioral science of programs like Vitality, the personalization of digital health, and the strategic alignment of value-based care. What is missing today is a framework that connects these elements into a unified, long-term system. Lifespan Insurance aspires to be that framework.

Conclusion

Lifespan Insurance is a simple idea with far-reaching potential: what if we built a healthcare system that actually wanted you to stay healthy? By rewarding prevention, aligning incentives over decades, and putting data and decision-making in the hands of consumers, LSI offers a new path forward. It won’t replace the existing system overnight, but it can run alongside it—filling in gaps, opening up new markets, and giving people more tools to live longer, healthier lives. Getting there will take smart policy, open standards, and a willingness to rethink some entrenched assumptions. But the payoff—more health, less waste, and a system that finally works for the people it's meant to serve—is well worth it.

I’d like to thank Jeff Chen for suggesting “Lifespan” (a change from the original name: “Healthspan”), Elizabeth Horn for convening a group to discuss the future of healthcare, and encouraging me to write this up, and Linea Avey for introducing me to the world of digital health, and the many conversations we’ve had on this topic.

Consumer added incentive:

Add lottery style rewards for those consumers in an LSI who get their do their preventive health care actions needed on their part. The more of their preventive health care actions that they do, they're more entries in the lottery system.

Could have multiple smaller lotteries or just a few larger ones. There might already be research that shows which variety is most incentivating to consumers.

-Colin